The title of this piece (pdf) from the New York Federal Reserve interested me, but now that I am reading it, the conclusions worry me in a different way! (my emphasis)

Relevance to Bankwatch: Mid sized banks will suffer profit pressure, unless they make some changes to their model.

These results hold for the most recent data and also back through the mid-1990s, when the number of branches in the U.S. banking system began to increase. Thus, recent technological developments such as Internet banking seem not to have altered the basic relationship between branch network size and performance. The one exception to this finding involves deposit interest costs, which appear to be systematically lower for banking organizations with larger branch networks during the mid to late-1990s.

“The impact of Internet banking has not altered the relationship between branches and …. performance”. This implies that Internet services have been added as an incremental cost, with no consideration to re-designing the overall channel mix.

Having grasped that, it makes perfect sense to me. Internet banking was generally treated as an annoying new expense and while most have overcome that now, the implication are that no-one is re-engineering the bank to leverage the potential from Internet banking.

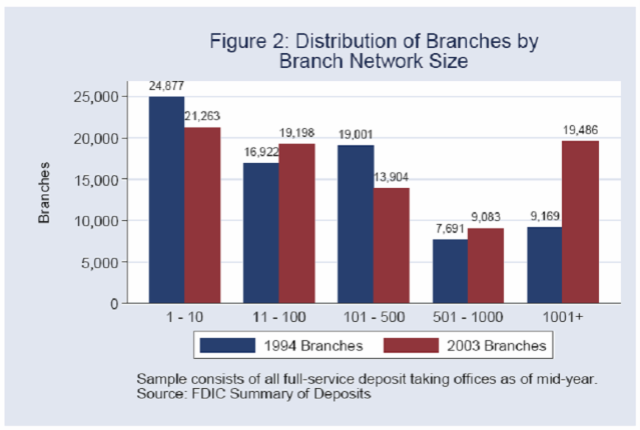

Mid sized Banks with 100 – 500 branches have reduced their network size in the 9 years to 2003, whereas the rest, smaller and larger have increased their branches.

The report then by page 24 starts to get at my interests.

The goal is to see whether the results discussed thus far – which suggest that mid-sized branch networks may be at a competitive disadvantage

relative to both larger and smaller networks – are stable over timeIn general, the implications of the historical results are quite consistent with those from the results

based on the 2003 sample.As compared to banks with the very largest branch networks, banks with midsized branch networks had lower deposits per branch, roughly equal volumes of small business loans per branch, but have historically had higher net deposit costs.

Banks with smaller branch networks (100 or fewer branches) had higher deposits and small business loans per branch than institutions with mid-sized branch networks, but faced higher net deposit costs.

The implication of these results is that mid-sized branch networks appear to be at somewhat of a competitive disadvantage, especially relative to the very largest branch networks, throughout this period. This disadvantage may have weakened somewhat in recent years, however, given the reduction in the difference in net deposit costs between institutions with mid-sized and larger branch networks

Their conclusions:

- Technological change has not altered the impact of branches on profitability

- Mid-sized branch networks have lower deposits per

branch than organizations with both larger and smaller branch networks. - Branches are on average, increasingly centralised in large firms

- institutions with mid-sized branch networks have no deposit expense advantage relative to institutions

with larger branch networks

Taken together, these findings suggest that banks with mid-sized branch networks may face profit pressure in their branch network operations since their per-branch performance appears to lag that of both smaller and larger institutions

From what I can see, the experience in Australia is much the same, but the definition of “midsize” here is a little smaller. We have 4 major banks with truly national networks and then another 5 or 6 that could be called regional, or mid-sized, and then down into the smaller mutuals.

The mid-sized banks are at a disadvantage on the liability side – deposits per branch are smaller. On the asset side, however, they tend to do better with the lending rates to small businesses, compensating for their more expensive funding. It might pay to see if the same is happening in the US.

I feel it is because smaller businesses feel more comfortable in a smaller bank, but this is just my feeling, although some surveys have backed this up in the past.

This would account for the stable position over time. If not, you would expect a gradual degradation in the position.

Great feedback – thanks ozrisk. It suggests to me that midsized banks then, in theory, have the opportunity to redress the imbalance in deposits per branch, through reduction in branches, if they can maintain customer loyalty, by better leverage of technology investments, particularly online. Its a hypothesis.

Please i need more information