Tara does a nice job of describing the root difference about understanding the new marketing. I like the point about going past the client, right to the clients’ clients.

It’s time to tip the scales, I think. I wrote a little post over at the CA Blog about our core philosophy and why we are more concerned with our clients’ clients than our clients. In a world that conspires against the ‘consumer’ (‘buy our stuff and shut up’ and ‘we care about you, really, okay we don’t, but we’ve paid a lot of money for this creative, so that you will think that, when we really should have put the money into replacing those crappy parts or empowering customer service to help you’), we are betting the bank on consulting our clients in the other direction.

Source: ::HorsePigCow:: marketing uncommon: Fake Blogs and the State of our Economy

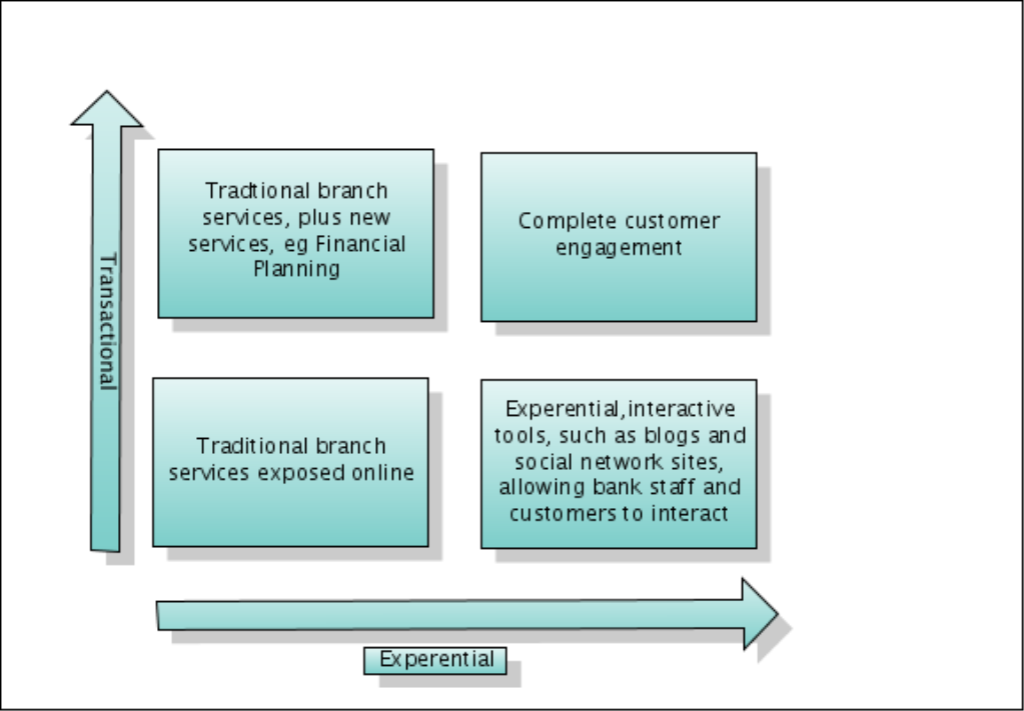

This is timely with our discussion about Building the Bank of the Future. In my poor attempt at a picture (I need help Tara), the point is that Banks cannot make it by restricting online acidity to automation of Branch transactions. This does not deal with the emotional side of the customer relationship equation.

If that experiential line is not done with heart, and merely replicates old marketing, then that Bank is done for.

Relevance to Bankwatch:

Social networking is critical, but will require CEO approval, and fundamental culture change at most Banks.

I guess the biggest question is: what do people want from their bank? I mean REALLY want from their bank.

Higher interest? Lower fees? Security? Help with finances? Personalized service?

I really do love banking in smaller branches, because the people there know me and are willing to ‘bend’ the rules, like 10-day holds on checks and stuff like that. The whole, “Hey Tara…yeah, we know you won’t skip the country. We’ll take that hold off.” That makes me feel very special. That phonecall when something odd happens in my account is amazing, too.

For others? I don’t know. That’s where I would start thinking about it. On the micro-level. The macro-level is astoundingly difficult.

Tara … thanks for the comment.

Yeah, your paragraph epitomises customer experience perfectly. The automaton Bankers want to find ways to do that with computers, but the information base that exists can never replicate that ‘small branch’ experience. I have been there, and its incredibly satisfying from the Banker persepctive too, when you see “Tara’s” expression and relief in knowing its all ok.

But I still wonder why Banks have to have such apparent life and death power over customers. That doesn’t seem right either. In essence that local banker is the middleware, between the big bad bank, and the customer.

You raise a good point though … social stuff won’t address the fundamental relationship point. This is yet another dimension.