Dave makes a clarion call post wondering why the obviously simple technology solutions don’t get traction.

What’s the barrier to doing this? The cost of generating a certificate for me to download is, to all intents and purposes, zero. It must be that it’s just too complicated: telling customers put in your card and punch in your PIN is one thing, but trying to explain to them how to download a certificates into a browser, after all these years, is another.

Source: Digital Identity: Federation in Nice

The best answer I can provide is this … I live in the Quixotic world between pure business leaders, and technology implementers/ architects. Welcome to my world is all I can say. There are two problems:

- customers: if its a different service, they just don’t need it

- bankers: if its not a new product bankers, don’t recognise it

With tongue firmly removed from cheek, the fact is that technology change for technology sake will never get traction in my view. That’s why beta tapes lost out to VHS despite being better, or why Apple computers have minimal market share despite being better. We can debate those in the comments, but facts are facts.

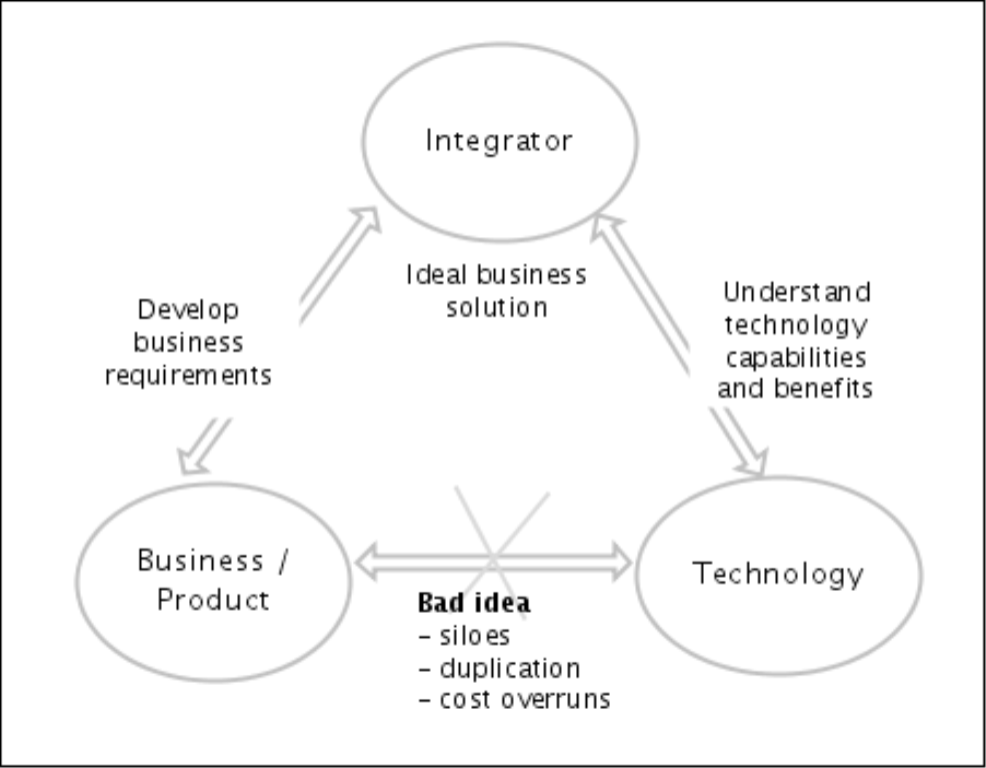

Technology in itself will always be an enabler, and so us guys in the middle, (look in the blogroll, and if you don’t happen to be there, then I am sure you know someone who is) have the un-appreciated task of being the translators to make the connections, and align the right pieces of the moving parts at the right time.

I have always figured that a competitive differentiator in a previous life was the ability to have technology and business resident in one person. This is the land of the good consultants, that can bring together the business strategy, with customer trends, and align with the appropriate technology capability.

Technology strategy for its own sake will end up as a bunch of powerpoint decks in a bank. It can never be funded unless there is a business case which will always be predicated on customers (revenue generation) or bankers (cost reduction). So here is my take on that. The ‘integrator’ can be a permanent consultant approach (CitiBank), a customer focussed group (Bank of America), a powerful channel group (Wells Fargo).

Key point here is the product group, and that’s the Banks’ Achilles heel. The President sees customers but he is too high to define business requirements. The product group see all the revenue and costs, and take that to the President, and there is the revolving door. The customer gets lost there every time. The optimal technology view gets lost there every time because the conversation vacillates between affordability, and new revenue. There is no room to discuss “optimisation”.

So looping back to Dave’s point, the “industry standards” piece which I think is a large part of his post must be dealt with by a combination of the integrator, and the technology people. They will drive out the benefits, and understanding of the customer benefits that will come through.

Thoughts? I know the picture needs work, but there must be a simple way to describe the solution, because Dave’s post highlights the solution, yet we collectively are not jumping at it.