I can safely say I have lived through all the mistakes and flawed assumptions since the beginning of online banking, when we simplistically spoke of the near future where marketing was as simple as the right message, at the right time, to the right customer.

I like James blog because he talks about how we should just do it based on what he calls EDM.

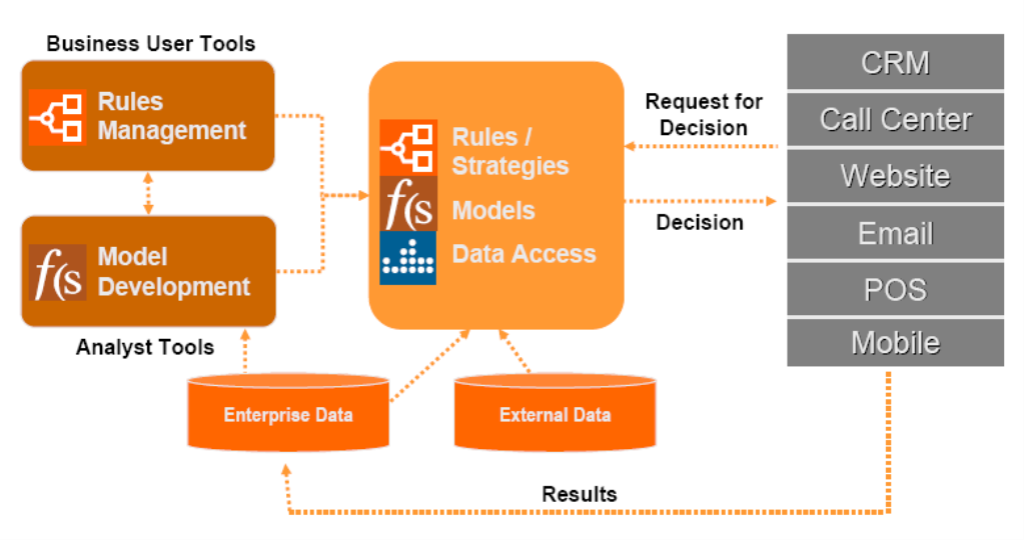

Essentially I proposed that using technology like business rules and analytics to improve the moments of decision when interacting with a customer can improve their experience. Targeting, rewarding loyalty, empowering staff and leveraging information are all part of this.

This evolutionary path is fascinating. The devil is in the details. I know from experience having seen Banks spend multi millions, yet fail to achieve the dream.

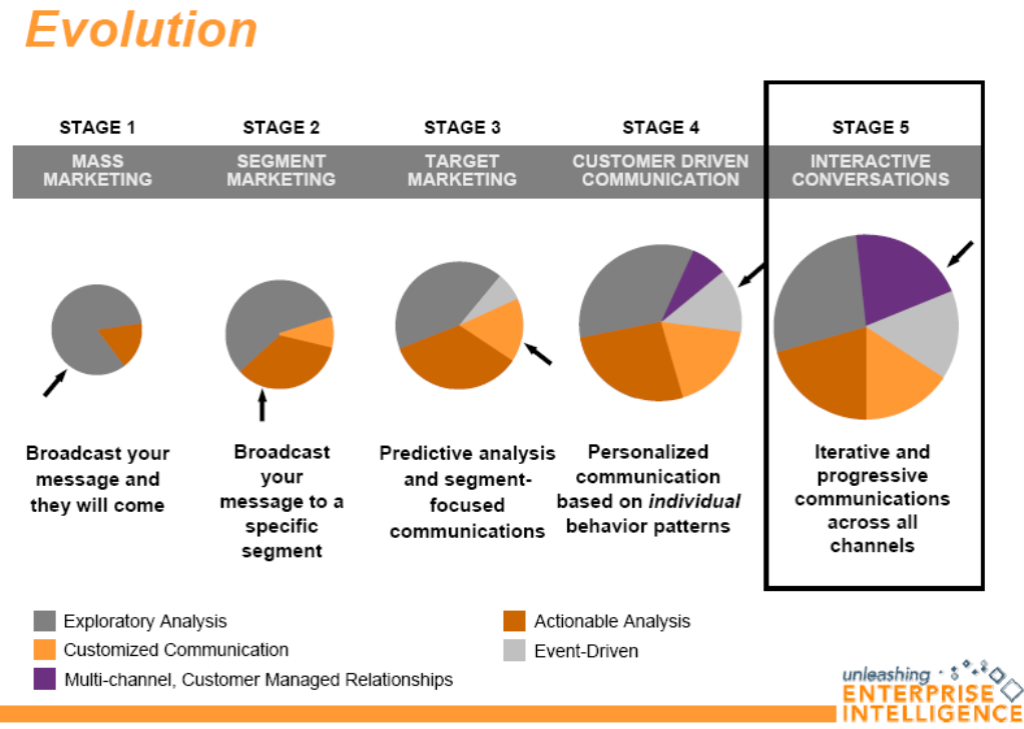

What I like about this model is the evolution of several components:

- exploratory analysis

- customised communication

- multi channel managed relationships

- actionable analysis

- event driven

Whether we agree on the components is neither here nor there. The point is that in 1999, the components were only # 1, and #5. The gradiency of 2-5 is what makes this a much more intelligent model, that has a chance of success. My personal space is #3, and it always felt like I was speaking ancient Greek to #1, and #5 because number 2, and number 4 were not there.

Now let me contradict myself, and throw in a new problem for EDM. By definition, EDM is decision based, that is, Enterprise decision based. I question how that factors in the customer decision process, based on external influences, community based opinions, and generally external influences. This is a very real matter now, and marketing is no longer as simple as how the Enterprise appraises he customer potential.

This from the deck, does have “external data” as a component, so we need to understand that.

For example, an internal decision process not matter how sophisticated, that predicts say, a line of credit, for a customer, is diminished in value, if that customer has reviewed lines of credit amongst banks, and prefers the stability of a loan, because a loan suits his personality. Another example could be a customer who has compared banks, and values convenience that DF Bank provides, yet your Bank is predicated on value added advice. He doesn’t need advice. How can we factor that behavioral aspect into the equation? There are probably better examples I should think of, but generally, I am asking how the external influences that customers are more and more receiving through communities of interest can be factored into the decision process.

Anyhow, the whole deck is here, and I do recommend it.

Technorati tags: marketing, 1-1+communication, personalization, pinkomarketing

Thanks for the kind words. You pose a great question that I try and answer in this blog posting.

http://www.edmblog.com/weblog/2006/11/the_customers_i.html