Brad at Forrester talks about the customer buying process, and how Banks’ need to do a better job understanding that process, as it has changed with online.

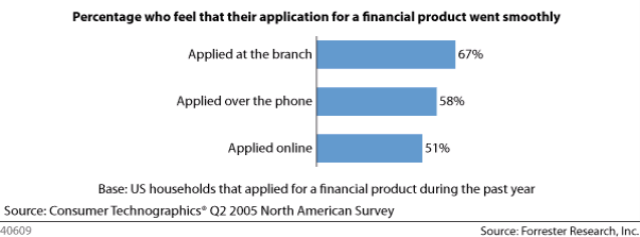

Financial services Web sites fail to meet customer expectations when compared with the branch and phone channels. Why do sites fail? Most financial firms do not understand their customers’ needs, their expectations, or the basics of online selling.

To drive more online sales, financial services firms must first understand what drives consumers’ choice of product. Armed with this information, they should create sites that deliver compelling content, decision-support tools, and a superior buying process to help consumers make a product and channel choice that meets their goals.

Source: Forrester Research

Integral to the dissatisfaction level is the failure to meet customer expectation.

It should only make sense that the online offerring should beat the others, yet the opposite is true. Banks have yet to understand the medium, and develop online applications that satisfy customer expectations. This is the next level.

Colin, I couldn’t agree more. Think about the in-branch environment and how the setting/architecture at many FIs are soft, friendly, and attractive. This comfort leads to happy customers.

Contrast that with the cold, functional, unfriendly feel of most online banking apps, and you can see why the frustration’s there for consumers.

Web 2.0 is bringing pleasurable user interfaces, conversational copy, and personality to other industries, and you’re right – FIs as a whole don’t quite get it yet.

Understanding the medium will surely have the online offering beating the offline in customer satisfaction for FIs who invest in treating their interfaces like they do their branch settings. The convenience element’s already there, after all.

I think banks will struggle with making their websites effective unless they both focus on the interaction and on automating decision-making so that the web channel can “decide” about loans, products etc. There was a stat in the report about the need to get approval while online without having to wait or come back. That requires decision automation and decision automation will, as a result, improve the customer experience.

http://www.edmblog.com/weblog/2006/09/live_from_terad_1.html

Interesting….I’m a huge fan of online applications, and believe they will outnumber branch apps by a large margin 10 years from now.

But as these numbers show…there is still much work to be done. In my testing, I have applied online dozens of times and have had some horrible experiences. More than once, I’ve submitted an application and never heard from the bank again, including one last year for a WAMU checking account, which should have been relatively routine.

Colin, are there any other factors at play, besides the channel, that may account for the satisfaction differences? Age, experience, income, etc?

Colin,

If you have not seen this yet, I thought you may be interested.