Another good piece from IBM. The premise is that ” To distinguish themselves, banks must look beyond new product introduction and spread accountability for innovation throughout the organization.”

Retail banks can’t assume that the growth and returns of the recent past will continue. Amid a throng of banking competitors – including new market entrants, forward-thinking incumbents and non-banks – banks need to differentiate themselves in ways that are not easily duplicated.

To restore confidence and realize strong future returns, banks must set the stage now. It will require uncommon innovation to stand out from the crowd and adapt successfully to marketplace demands.

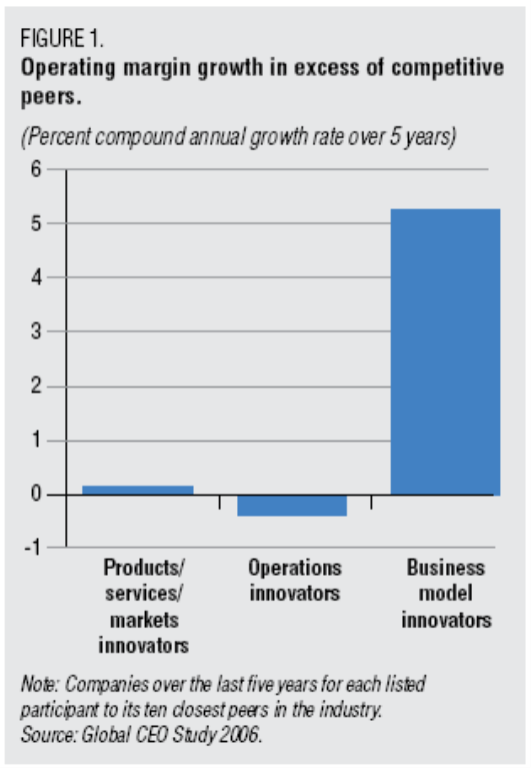

Assuming that differentiation stems from innovation, they studied three types of innovation.

Three types of innovation were evaluated as part of the study:

- Products, services and markets – Develop new products and services, target new markets and audiences

- Business and enterprise models – Refocus, restructure and extend the enterprise

- Operations – Improve effectiveness and efficiency of core functional areas.

And the results were no surprise – business innovation wins out handily.

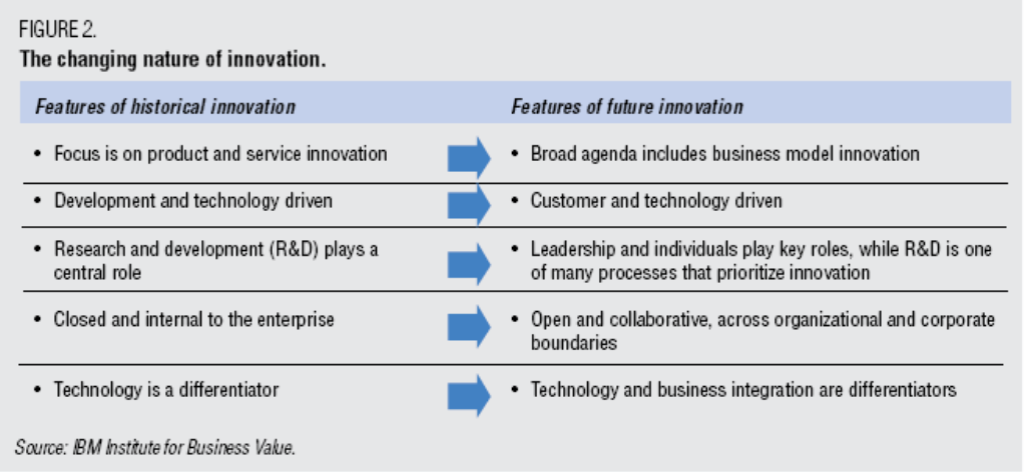

Then there is the nature of innovation, as banks move beyond old fashioned product innovation:

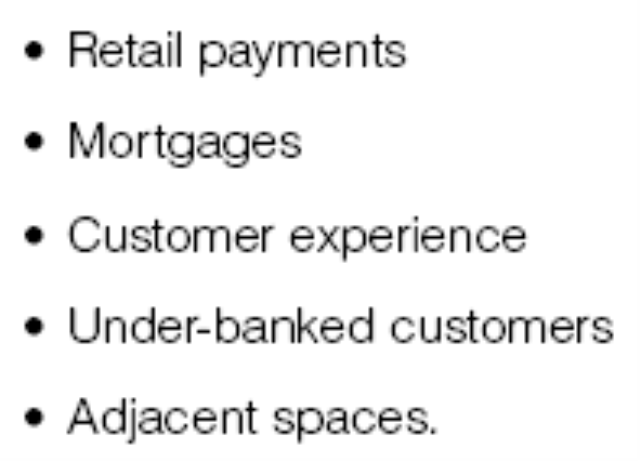

Areas of the the business in which to innovate come next:

I will focus a little deeper here on the less obvious three – my personal favourite -customer experience, underbanked, and adjacent spaces.

Customer Experience

A stronger focus on customer experience should enable banks to raise the industry’s 70 percent customer satisfaction rate and reduce the 24-month turnover rate of 50 percent.

Examples provided are:

Leading customer experience innovations include:

- Loyalty programs

- Enhancing branches to engage the community and increase sales of bank products

- Customer relationship management (CRM) and personalization

- Product integration (what others might call product bundling)

I don’t buy the examples under CRM/personalisation as being very innovative. Personal messages at the ATM is simply a capability that now exists due to technology, not due to a rampant customer need to interact at the ATM more than to get cash. The other examples are good.

Under banked

Today, new technologies enable cost-effective ways to serve the over 3 billion “unbanked” adults in emerging and developed markets.15 Banks are discovering the profit potential in reaching these groups when services are provided to them differently.

I have covered this area before. Walmart are going after this group as a segment. No signs of Banks heading there yet. While Banks are entering the international personal remittance market in droves, that is more an ethnic play, and not an unbanked play.

Adjacent Spaces

This one is interesting, because its new and different.

Examples provided are:

- Healthcare savings accounts (US)

- Electronic Payment processing (the Aneace theory – personalisation, and innovation at the point of customer transaction contact)

- Electronically integrated procurement, invoice presentment and payment (EIPPP)

- Electronic bill presentment and payment (EBPP)

Relevance to Bankwatch:

All in all a medium rated paper. It starts off well, and I liked the broad categories of innovation (retail payments, mortgages, customer experience, under banked, adjacent spaces) but the innovation examples within those categories felt like a let down to me.

But I understand the reason too … its hard to develop examples that are innovative, and make money at a pace that keeps the markets happy.

Worthy of a follow up post to put my money where my mouth is!