NetBanker covers the introduction of two new high rates savings accounts, and see the post for the success of their first day.

# E*Trade Bank: Its new 5.05% Complete Savings Account was advertised in the Wall Street Journal today

# iGoBanking: The new online brand from Flushing Financial launched Monday with a 5.3% rate

Source: NetBanker 2.0: E*Trade Bank and Flushing’s iGoBanking join the 5% online savings account club

This is an opportunity to review their offerrings. Other Banks – watch out – this is good stuff.

- no minimum deposit

- no account fees

- no ATM fees

- open an account/ credit card online immediately

- full security guarantee

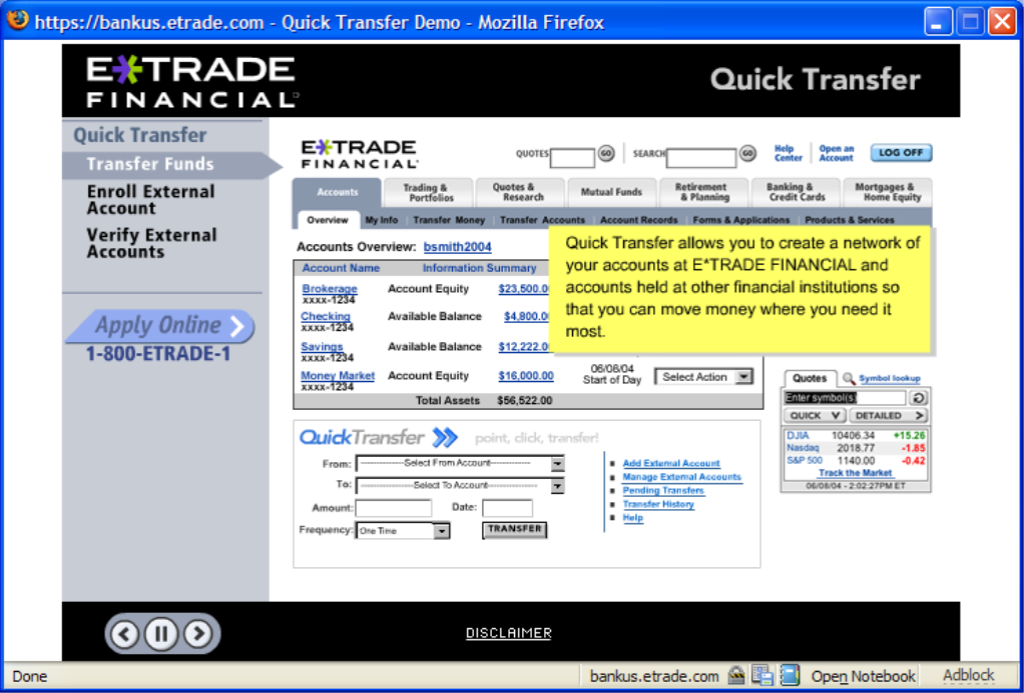

- fabulous demo

- boring colours/ design, but highly functional and clear, in the same way ETrade revolutionised brokerage; screen shot of the demo underway below

Conclusion: rich in capability and functions; price is the ‘hook’ – the experience will keep customers

- nice use of colour/ photo

- promotes simplicity

- no fees, no minimums

- weak on explanation and no demo – presume that is coming

- needs work, but I will come back and review – attractive enough to interest me

Technorati tags: online+banks, online+banking

I signed up several weeks ago for igobanking.com and transferred some dollars from one institution, Amsouth, to iGoBanking.com.

During the transfer process I got nervous because it said “click here for fees for transfer.”

I clicked the link and it opened a new window where all it explained was transfer limits. I looked through FAQ and all over the site where it explained the transfer fees (not mentioned anywhere).

I sent an email last Friday with a ‘read receipt’ attached. The email was read Monday morning. It is now Wednesday night and I still have no response. I sent a follow up email this afternoon and got a read receipt, but still no response.

I am concerned that this is an example of there customer service and it makes nervous and putting my money there.

I called, and did get an answer. The woman spoke English very poorly, wasn’t very polite and seemed annoyed that I was asking her questions about the fees, which she said there were none.

Of course we all have probably had experience talking with “John” at some big company who has no way to reach him or extension to hold him accountable to what he says.

Apparently there are no fees right now, according to this one person. But it isn’t clear on their site, and no one responds to emails.

Not sure I want to put my money there. Emigrant Direct might be a few points lower on the rate, but they respond quickly.

Justin, thanks for sharing your experience. I was considering moving several accounts there, but now I’m not sure. When you’re not dealing with a brick and mortar establishment, it’s really important to know that the online business has EXCELLENT customer service. No response or a lukewarm response is not acceptable.

Justin/ Robin … this is the right debate for Direct Banks to pay attention to. I hope there are still not Banks there that think Direct Banking is as simple as opening a web site.

The expectation is justifiably higher for Direct Banks, and those that do no exceed expectations will fail, and potentially take the mother bank with them in terms of customer satisfaction.