OpenId is a digital identity system. It operates by keeping your identity securely with you, yet permits you to log into participating applications. You control your identity, your information, and the degree to which your information is shared with the application.

This article explains the benefits of OpenId when compared to others in the same space.

- OpenID is a fully decentralized system.

- OpenID has a much lighter cost structure than any alternative.

Source: » The case for OpenID | Digital ID World | ZDNet.com

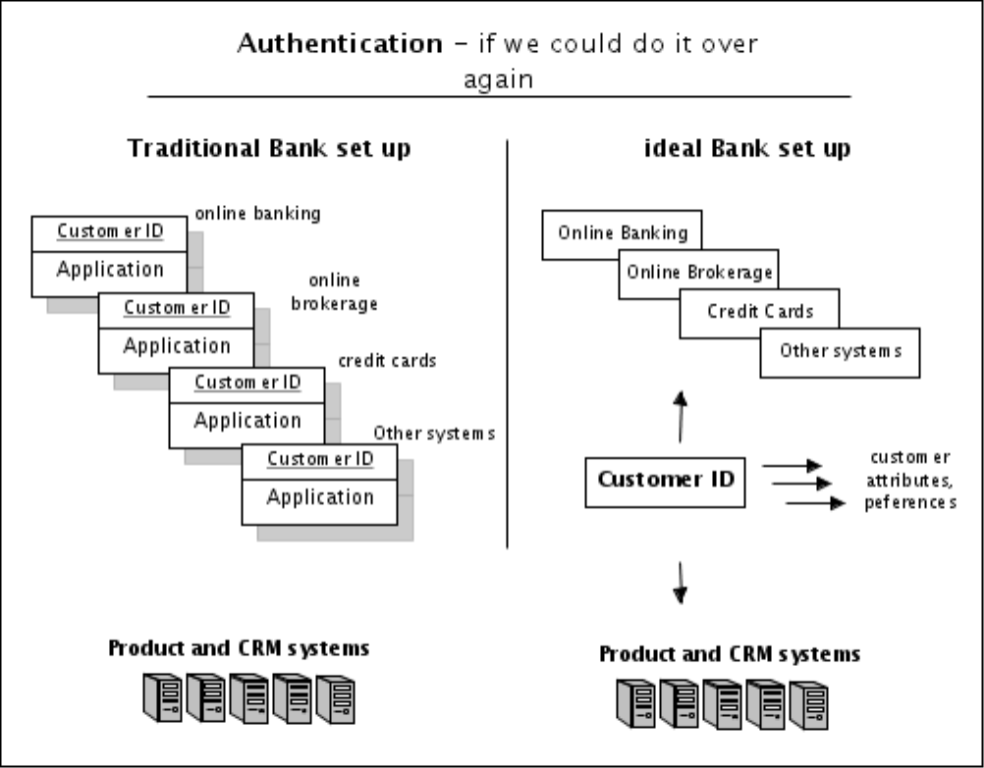

Its an important concept. Consider your Bank … online banking, credit card system, online brokerage, cash management system, private banking, mutual funds etc etc – all separate applications, each with their own customer authentication built into the application. This is one (of the many) reasons that its very hard to aggregate customer information in a meaningful way that supports Customer Relationship Management for self service channels at Banks.

The concept that OpenId is the antithesis of that approach. In an idea scenario Banks would have implemented a discrete authentication method, standalone. That method could then support each of the various applications, including the CRM system. It would be …. customer centric.

The concept is that by keeping the customer ID separate, it can be easily adapted, and informed by preferences and other attributes. Examples of preferences would be mainly generated by the customer themselves, and ideally through self service. This could include for example:

- don’t call me at dinner time

- don’t ever phone me

- email me

- contact me only once a year

- contact me only about mortgages

- etc

Attributes could be bank generated things like customer segment, and marketing potential. When we take the preferences and attributes together, we start to get a picture of how we should interact and work with that customer for their benefit, and the Banks benefit.

When the customer ID is tied into many systems it is much more complicated, and exponentially more expensive to address preferences and attributes for all systems.

While progress is being made, most banks lean towards the left diagram, and this is why the customer experience is often fractured. How many people have a CapitalOne credit card, and still get telephone calls trying to sell them a CapitalOne credit card! I pick on them because they are flagrant about it, but they are not alone!