Alex Osterwalder at Arvetica posts about Bank branch architecture, and please go there for that. What I wanted to capture here was the premise those smart folks used for six different bank models. Professor Jeffrey Huang’s class runs this summer at

…

![]()

… in Lausanne, Switzerland.

The first thing that struck me was the the traditional bank is not on this list. hmmmm

- The Art Bank in Zermatt (see above image), where customers (presumably wealthy private banking clients) could do banking while admiring an art exposition. UBS served as a starting point to the reflections.

- The Adaptive Bank that is present at different locations based on the population’s weekly routines of commuting, working, leisure and weekend. The concept was based on Raiffeisen’s business.

- The Bank as a Restaurant where customers get served a banking menu and where quick transactions are done in a fast-food area. Postfinance was the starting point for this concept.

- The Bank as a Forum, which is the physical branch of an online bank. Its purpose is to cater to the needs of a community of practice of active online traders and investors. It brings a physical space for knowledge exchange to a community mainly dominated by online routines. Swissquote was at the roots of this idea.

- The P2P Bank as a marketplace, where anybody can lend credits to borrowers – the banker actually disappears. This concept was based on the online peer-to-peer lending platform Zopa that eliminates the need for a credit banking intermediary.

- The Second Life Private Bank, which is the branch office of a private bank in the virtual world Second Life. The largest Swiss private bank Pictet served as a basis for this reflection.

Source: arvetica : Blog Archive : The Architecture of Banking

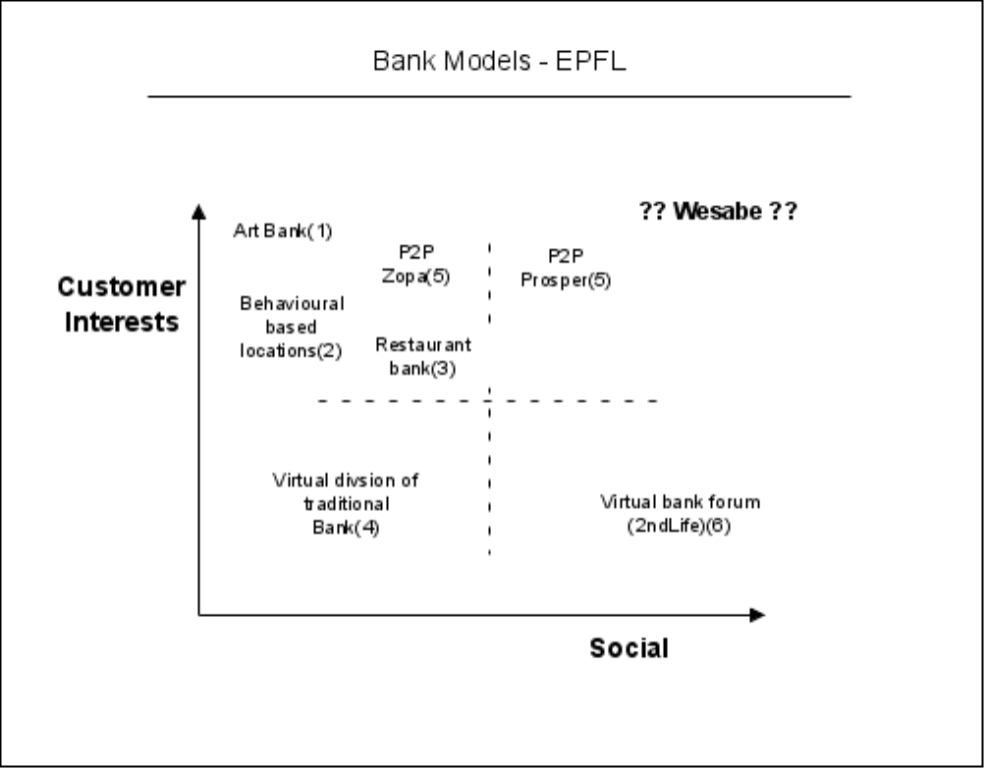

I have attempted to place those models into a matrix to establish the differences, and alignment with the ultimate (top right ) solution. Social within my definition, refers to interaction capability, customer –> customer or customer –> employee.

This is directional, and how I read the descriptions above. The numbering aligns with the descriptions.

If I were to place traditional banks on this it would be mid high (left/y axis) left (lower/x axis). Today’s branches are placed based on population density and potential, which moderately reflect customer interests, but has zero social aspect.

In depicting this view two things struck me:

- P2P has many alternative implementations, and I used two – Zopa which is customer based/ lower on the social scale, and Prosper, which is more social, but still customer focussed

- Most alternatives are customer segment (read organisation) focussed

What struck me here, and this is my perspective, is that its easy to gravitate north up the Y axis, thinking that segmentation is in the customers interest. It may well be in the customers interest. However the test would be the social aspect. Social could be with the organisation, or with other customers, or with both. I make no assumption here. I do know that most segmentation plays by Banks have weak links to the employees, so the customers is left to fulfil by themselves, alone.

I stuck 2nd Life bottom left, and I would place MySpace there but lower on the y axis. Social for socials sake is a non-starter in my view. There has to be a raison d’etre.

Lastly I made the leap and placed Wesabe in the upper right. It fulfills the role of full fledged social site, as well as addressing customers interests head on, whether creation of a will, or help with budgeting.

Thoughts and views welcome !