")

Even though the number of banks in the US has reduced to 7,402 at the end of last year from 14,411 banks in 1977, there remains a significant opportunity for community sized Banks to compete. They can bring a customer focus and clarity of vision that is hard to accomplish in larger institutions. This is evidenced by new ones being set up every year. (Hat tip Neil)

A small bank is the vein that carries blood to the heart, said Edward Carpenter, chairman of Carpenter & Company, an investment bank that in 33 years has organized the founding of 708 banks in California and across the United States.

Source: Countering the Big-Bank Trend – New York Times

This article articulates well the reasons with a key one being technology oddly enough. Once considered the prime advantage of the large FI’s with their mammoth budgets, the tables have been turned with a combination of off the shelf solutions available, along with home grown solutions.

Here are two examples I have noted recently in conversations with others, that demonstrate the two ends of the spectrum that are available:

- Cashedge: provides a comprehensive capability for online account opening, including identity verification, e-documentation, and account funding. This is used by many of the offers for high interest online only savings account offers.

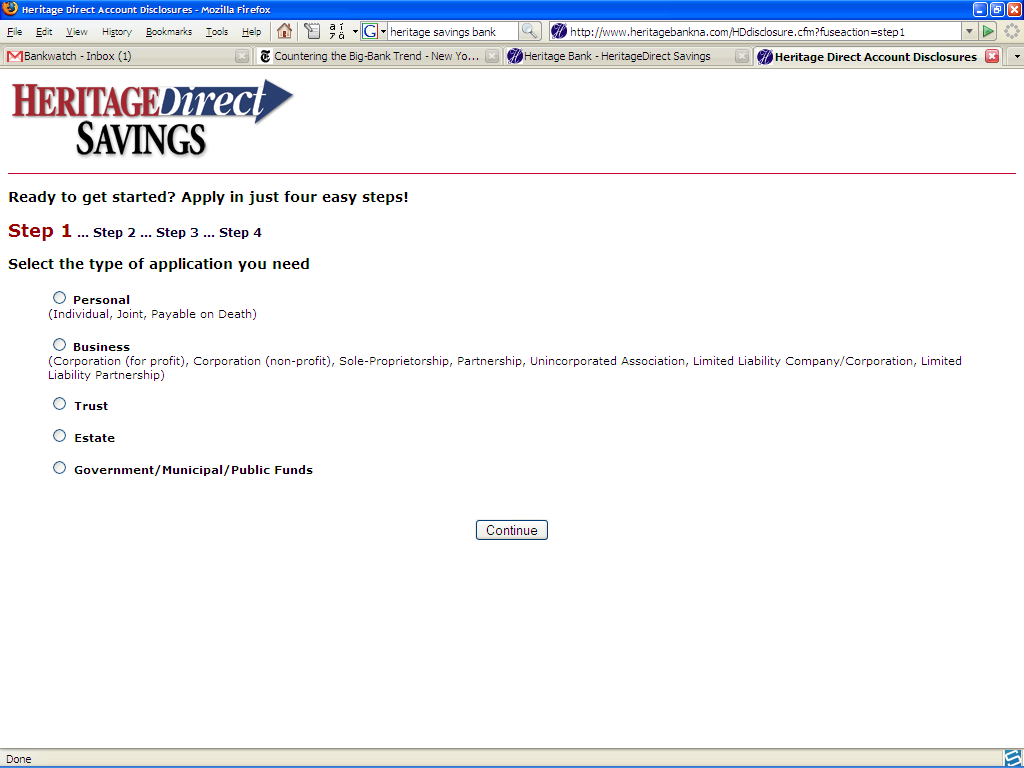

- Heritage: what appears to me to be a home grown online application, that is very slick and simple. Its a four step process, and 2 of the 3 are “agree to terms and conditions” so its very fast. From my own observation of the application, it looks like this one was built by Heritage. So this is a great example of the opposite end of the spectrum from the Cashedge approach. Less sophisticated in terms of functionality that might require more manual intervention, but very smooth and simple for customers.

Heritage is four steps to get you to the right application, so maybe not “very fast”.

Technically you are correct Matt, but I give them an ‘A’ for effort. Even though you have to click 4 times the first 3 are low impact.

You raise a great point though … the first three clicks are obviously driven by mainly legal input, plus a more traditional process approach (no disrespect Heritage) thats typical of Banks.

I couldn’t understand, how you overlooked the variety of methods provided by CashEdge for facilitating the user before giving ‘A’ to Heritage.

CashEdge is providing top of the charts services for Online Account Opening in US banking market.

Nitesh … I presume you have a vested interest in that comment, but you have provided no link to your site.

If there is more information relative to my post or the the several mentions of Cashedge I have already made, please let me know.

Check out this link for my earlier nine mentions.

http://thebankwatch.com/?s=cashedge

If only there were a Canadian equivalent! While online account opening and funding is very widespread in the US, our different rules/requirements around account opening create obstacles to offering a completely online version in Canada.

Pierre … what do you believe the hindrance in Canada is? My own experience suggested most of the hold up was our own internal rules.

Hi Colin… more regulatory (Fintrac) than internal from my experience.

I expect these regulations to ease a bit overtime, and new legislation will be proposed as satisfactory technology alternatives become more widely accepted.