")

Two very thorough reports from Oliver Wyman.

New Monetary Order

Key Policy Issues in Finance in 2023

THE SHORT VERSION

- For those of you with less time, here’s a summary version of the points.

- THE NEW MONETARY ORDER

Policymakers and financial executives are striving to understand what the future shape of the financial sector will be as the period of “low for long” interest rates recedes further in the rear-view mirror. This requires making sense of at least four broad trends, the interactions between them, and the practical implications of that understanding. At a minimum, these trends are:

- Higher and more volatile inflation and interest rates

- Smaller central bank balance sheets

- Stronger constraints on central bank interventions in financial markets

- Shifts in market share between banks, non-banks, and financial markets

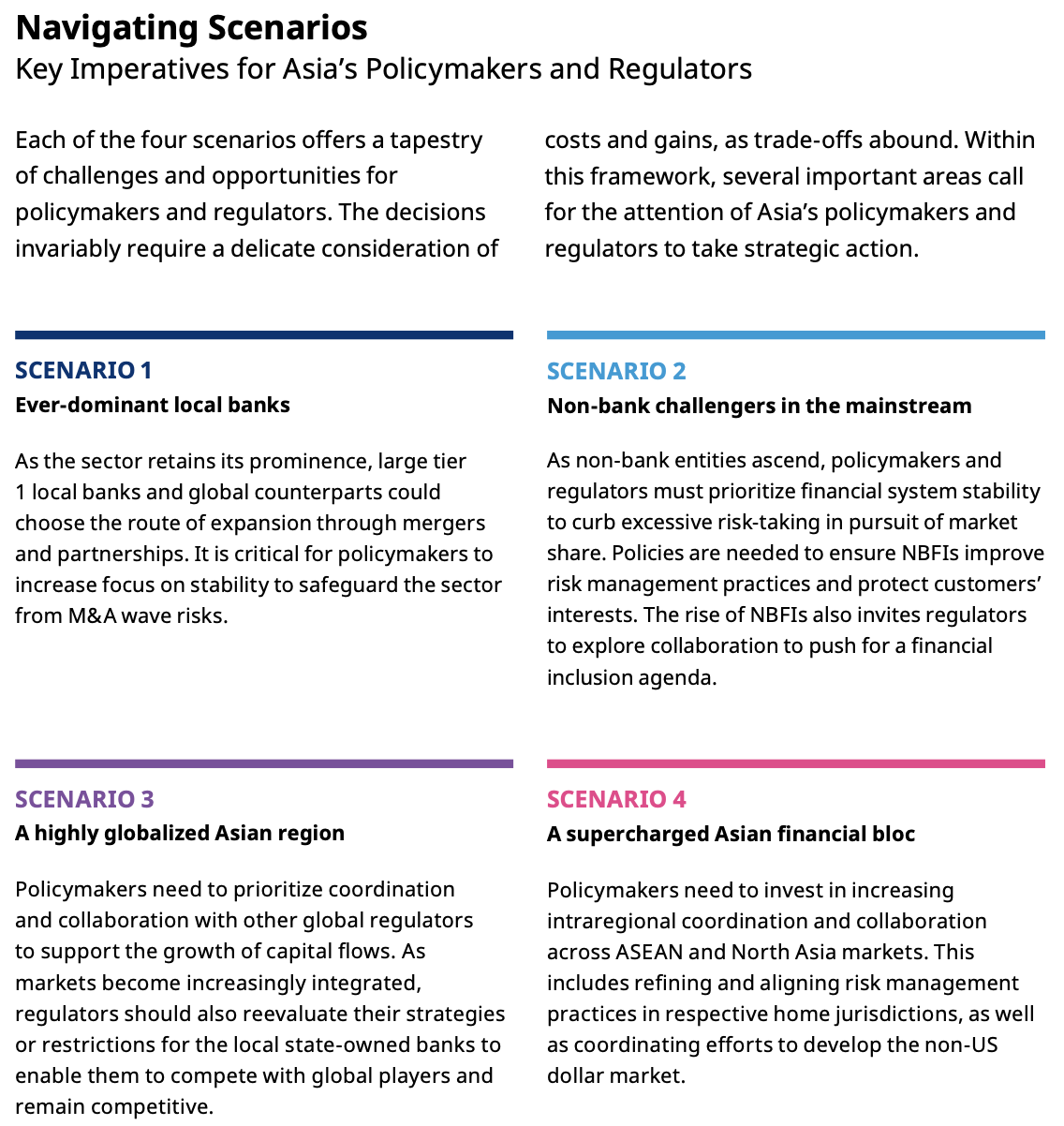

Given the impossibility of predicting the future, the best analytical approach is scenario analysis. One interesting potential scenario would see banks regaining some of their lost market share from non-banks and financial markets, since wholesale and market-based funding has ceased to be nearly free and readily available under virtually all circumstances.

This meta-theme is particularly complex, so please do go to the long version for a deeper explanation.

MARKET FRAGILITIES AND REPRICING OF FINANCIAL ASSETS

Policymakers have two broad classes of concerns about financial markets. First, some ultra-safe assets, such as US Treasuries or UK gilts, trade in markets that have developed structural fragilities. Policymakers are aware of these risks, but have not reached the stage of fixing them, given the complexities and constraints. Second, policymakers tend to believe that many risk assets are substantially over-priced, not yet properly reflecting the underlying risks or the new interest rate structure. I agree, but it must be admitted that I share a conservatism with most policymakers that could bias our viewpoint. In any event, if this view is correct, then there is a substantial risk of a sharp repricing at some point as reality seeps in, which could produce financial stability problems in various ways, including the potential for multiple blow-ups similar to what Archegos suffered.

CREDIT RISKS

2023 could be the year in which credit losses start to bite the financial sector in a serious way. Policymakers have a keen eye out for risks from all major categories of borrowers: households; businesses; and governments. At the beginning of 2022, there was much less concern about household solvency or that of most governments outside of a few emerging market countries. These concerns are now more general, given much higher interest rates and considerably greater risk of recession than was perceived a year ago.

GEOPOLITICS AND FINANCE

The Russian invasion of Ukraine and its many economic consequences has considerably increased policy debate about the impact of geopolitics on finance. The war in Ukraine continues to be a source of further potential macro-economic shocks, positive or negative, including the possibility that peace might break out at some point. The other major focus is on relations between China and the US and its allies, including the potential for China to move militarily on Taiwan or for China and Russia, with a few allies, to try to set up an alternative financial and economic grouping separate from the existing global structures.

DIGITAL ASSET POLICY, REGULATION, SUPERVISION, AND ENFORCEMENT

Digital assets will continue to consume large amounts of policymaker time and attention. The debates in 2023 will be considerably influenced by the disasters of 2022, including: Crypto Winter; the blow-up of the Terra/Luna algorithmic stablecoins; the bankruptcy of firms taking quasi-deposits and lending them to risky crypto asset players; and the scandalous FTX debacle. A few things seem clear;

- Digital assets will not go away, in large part because there are many sub-sectors that are quite removed from the parts of the ecosystem that blew up

- The healthy sub-sectors will continue innovating rapidly

- There will be major moves to regulate digital assets much more widely and strictly

- Crypto exchanges and similar service providers will find themselves under regulation similar to traditional financial exchanges and custody providers, although this may take several years to come into force

- One thing that is not clear is what the price level of Bitcoin and similar cryptoassets will be and what level of investment and speculative interest there will be. Prices are down a lot from peaks, but already bounced back 30% or so from the lows. The lack of underlying financial flows (such as from the earnings of a business or interest and principal payments on a loan) makes pricing much more dependent on investor sentiment than with most financial assets.

CLIMATE-RELATED RISK AND FINANCE

Policymakers globally continue to advance the agenda to reflect climate-related risks for financial institutions. Regulators continue to push the industry to gather better data on these risks and have also put financial institutions through stress tests to better understand the size and nature of the risks. More broadly, securities regulators, such as the SEC in the US, are moving to require considerable disclosures of climate-related risks by all public companies, including financial institutions.

All of these trends will continue, although there has begun to be more resistance, partly because regulatory moves have become more concrete. Some of the resistance is based on overall opposition to the regulatory approaches, as from those who believe climate risks are smaller than generally perceived or that regulatory approaches are too heavy-handed. For others, the argument is that the current energy crisis requires a delay in these moves.

— —

APPENDIX

Oliver Wyman Oct 2023

Dear Reader,

The monetary policy context for the global financial system since the GFC has been low or ultralow interest rates in most of the world, an expansion of central bank balance sheets, and a significant program of regulatory reform.

This period has reshaped the financial system in profound ways, in terms of liquidity and funding structures, capitalisation, the level of interest rate risk in the system, and the growth of different forms of credit.

The period has also seen significant shifts in the roles of constituents in finance, with the growth of non-bank financial institutions, the rise of regional and domestic banks in some parts of the world, and the increasing challenges with cross-border and international banking.

Yet what does the future hold?

Whether or not you believe we have moved into a longer period of inflation taming, high interest rates and lower liquidity, it is clear that low-for-long is over and this represents a major paradigm shift which will undoubtedly also reshape the financial system in the coming years. Do we understand the possible scenarios before us? Do we retain the expertise in the industry to manage through these scenarios after two decades of low-for-long? Who will the winners and losers be?

In our State of Financial Services work this year on the New Monetary Order, we explore these questions. Our work will look at the dynamics of different regions and segments in a series of papers and conclude with our global perspectives. Here is our Asia Perspectives paper on the New Monetary Order. We hope you enjoy the research.

Sincerely,

Ted Moynihan

Managing Partner and Global Head of Financial Services