I have been thinking and listening about P2P/ social lending, and wondering exactly what is the outcome and to relate that to traditional banking.

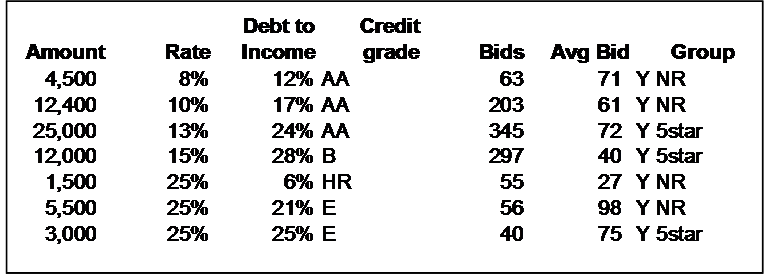

I took the first seven loans from Prosper tonight, and here they are. I re-sorted them based on the rate column.

The rates mapped to the credit scores. The better the credit grade, the better the rate. (I have to research what HR means, so I ignored that as an outlier)

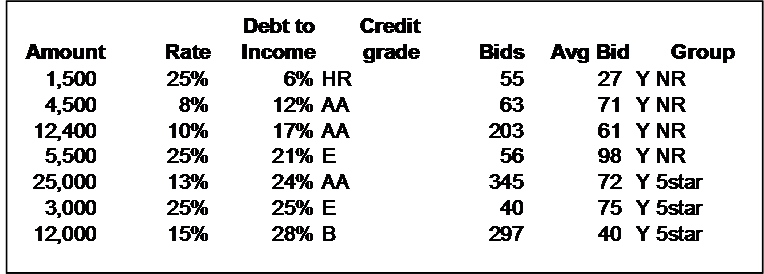

Then I sorted by Debt to Income … I expected to see the number of bids relate to this one based on lenders reducing their relative risk to that borrower. Wrong … there is no apparent correlation to that statistic. That is interesting to me, because that is the core attribute traditional Banks look at.

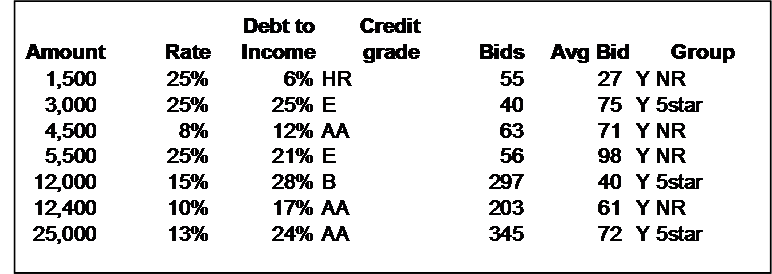

Then I sorted by amount, and still no correlation leaps out.

Final point here. For each of those rates, the rate shown is what the borrower pays, and what the lender receives. Prosper take 0.8% approximately (three year loan) so that is so small as to be un-noticeable. Basically the spread is almost zero. Banks make 5-6 % spread on many loans, and credit cards are off the scale.

So the lender return is very high in this model. Over time, I would expect lender rates to flatten out provided borrowers are good, and keep their loans up to date. In fact groups will come in to play, and insist on the effective bank spread benefit being shared between the lender and the borrower.

This is one of the beautiful things about this model. As that dynamic plays out (or not) Prosper are ambivalent … they can watch a perfect market sort itself out, and the winners are the particpants; the lenders and the depositors.

Relevance to Bankwatch:

Social lending might just teach us things. Being a banker I used primary Banker attributes in the spreadsheet. Bankers use them because they eliminate risk from poor judgement. The decision becomes more quantitative, and audit-able.

In Prosper, this tiny example suggests the correlations are not as expected, suggesting that their are other attributes coming into play, qualitative attributes, that lenders can bring to bear. The power of groups, borrower reputation, borrower loan purpose, borrower history and borrower lifestyle.

It would be too expensive for a Bank to use this methodology, but when the process is outsources to engaged, interested lenders, whose best interests are served by their own values a new model is born.

More analysis required, but I can see the some direction.

Technorati tags: social+lending, P2PLending, zopa, prosper

Interesting. I think that bringing some of these less quantative factors to bear is going to be a trend in the next few years, especially when focusing on under-served markets. As I said when you asked about this kind of area before – http://www.edmblog.com/weblog/2006/11/the_customers_i.html

From Prosper’s Website:

What are HR and NC?

HR = High Risk. These borrowers have a credit score below 540, which many traditional lenders consider to be high-risk.

NC = No credit score. These borrowers have no credit score because of limited information or no recent activity on their credit report. For example, a borrower with an NC grade could be a college student who has simply never had a need to borrow money before. It could also be someone who has had no activity on his or her report in the last 12 months.

Note: The HR and NC credit grades are named differently than the other letter grades because most lenders (like banks and credit cards) often won’t lend to people who fall in these categories. Prosper is different because all borrowers, regardless of history or credit grade, will have a fair chance at attempting to get a loan. It’s up to lenders to assess and assume the repayment risk of borrowers with those ratings. For example, a potential borrower with an NC rating could very well turn out to be an A-level borrower—there just isn’t any history to back this up. In these cases, a borrower’s group reputation is particularly important.

Thanks David …. the NC cases particularly for students, and people starting out are certainly one group that the Prosper model is well suited to help.

Colin,

Great article. I really feel it is up to banks/credit unions to start helping facilitate these sort of transactions within their institution or lose a very legitimate new revenue stream and continue to turn off and disappoint their customers in the process.

Evidently Prosper is moving towards developer tools and data mining resources (evidently released on 11/28 but I just discovered it while browsing the site tonight): https://www.prosper.com/public/tools/

Brad… I agree. Banks must find another way to enter this space otherwise they will be disintermediated in the personal loan space.

I would add, that the other side of P2P is the deposit aspect. The lenders in P2P lending are moving those deposits from bank accounts and brokerages. Banks are losing on the deposit side as well as the lending side.

David,

one example for the use of the developer and data mining tools is

http://www.wiseclerk.com

Especially check out the option to map a lender portfolio, which is something you cannot do on the Prosper site itself